Nasdaq Inc. has formally requested regulatory approval to extend trading hours for its single-stock securities to 23 hours per day. This initiative, driven by evolving investor demand and competitive pressure from the always-on crypto ecosystem, seeks to bridge the gap between traditional finance (TradFi) and the modern expectation of continuous market access. This article explores the drivers behind Nasdaq’s proposal, its technical and regulatory challenges, the profound implications for global market structure, and the undeniable influence of the cryptocurrency industry in reshaping expectations around liquidity and accessibility.

Nasdaq’s Request to Extend the Trading Day

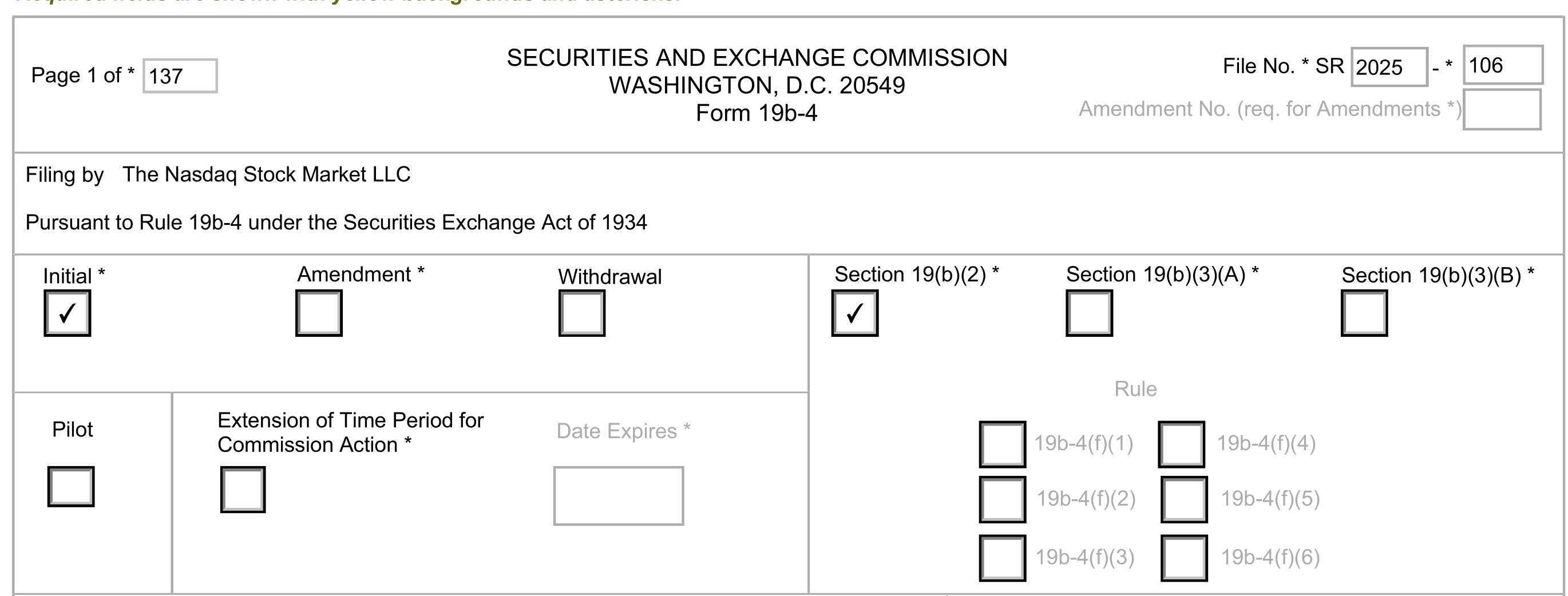

Nasdaq’s request to the U.S. Securities and Exchange Commission (SEC) is not merely an extension but a near-total dismantling of the conventional trading day. The plan aims to implement a 23-hour session for stocks listed on its exchange, running from 4 a.m. to 3 a.m. Eastern Time the following day. The sole break, a one-hour pre-market pause, would allow for necessary system resets and settlement processes. This model effectively creates a cycle where trading closes briefly only to reopen almost immediately, offering a framework remarkably similar to the perpetual operation of digital asset exchanges.

The core argument from Nasdaq is one of democratization and modernization. In a globalized economy, news and events impacting corporate value do not adhere to a 9:30 a.m. to 4 p.m. ET schedule. Investors in Asia or Europe must currently react to after-hours earnings reports or geopolitical developments in a vastly illiquid and fragmented extended-hours session. Nasdaq’s proposal would unify this into one continuous, deep liquidity pool. As noted in their filing, the goal is to “provide investors with additional flexibility and the ability to manage their equity portfolios in response to global events” outside the current window (Nasdaq, 2024). This directly addresses a pain point that retail and institutional investors have increasingly vocalized, especially those who have experienced the constant availability of crypto markets.

Why Extend the Trading Window?

The demand driver for this change is multifaceted. Firstly, the proliferation of electronic and algorithmic trading has created an investor base that expects constant access. Retail trading platforms like Robinhood have conditioned a new generation to view investing as an on-demand activity, similar to streaming media or online shopping. The volatility during the COVID-19 pandemic, where massive price gaps occurred between the close and the next open, further exposed the risks of a non-continuous market.

However, the most significant catalyst is the benchmark set by the cryptocurrency industry. Bitcoin, Ethereum, and thousands of other digital assets trade on a 24/7/365 basis across a global network of exchanges. This market never sleeps, allowing for immediate reaction to news and eliminating the weekend or overnight risk that plagues traditional equity holders. For a growing cohort of investors, particularly younger demographics and those with cross-asset portfolios, the traditional market hours feel anachronistic. The crypto market has demonstrated that continuous trading is technologically feasible and commercially viable, creating a competitive pressure on legacy institutions to modernize or risk being perceived as inefficient. Nasdaq’s move can be interpreted as a strategic effort to integrate this round-the-clock trading ethos into a regulated, institutional framework before a competitive gap widens further.

Technical and Operational Changes

Implementing a 23-hour trading day is a monumental operational challenge. Nasdaq’s infrastructure is already robust, but extending a main session imposes new demands. System resilience becomes paramount; a technical glitch in a 24-hour market could have catastrophic, non-stop consequences. The exchange must ensure nearly absolute uptime, requiring significant upgrades to redundancy and failover systems. Secondly, the human element of trading must adapt. Broker-dealers will need to staff trading desks for longer shifts or develop sophisticated overnight automation, increasing operational costs. Settlement and clearing cycles, currently tied to the traditional timeline, would require a comprehensive overhaul. The Depository Trust & Clearing Corporation (DTCC) would need to adjust its processes to handle settlements that originate from trades executed across nearly all hours of the day.

Furthermore, market structure dynamics would shift. Liquidity, which is currently concentrated in the core session, could initially become thinner during overnight hours, potentially leading to higher volatility. The role of market makers would evolve, as they would need to provide quotes for a much longer period, likely incentivized by new fee structures from the exchange. Nasdaq itself would need to manage the rollout carefully, potentially starting with a limited set of highly liquid securities, such as those in the Nasdaq-100 index, to ensure stability before expanding to all listings.

Regulatory Scrutiny and the SEC’s Dilemma

The ultimate gatekeeper for this transformation is the U.S. Securities and Exchange Commission. The SEC’s mandate to protect investors, maintain fair and orderly markets, and facilitate capital formation will be tested by this proposal. Regulators will have significant concerns. Investor protection questions abound: how will retail investors be safeguarded from increased volatility in thinner overnight sessions? Will the ease of access lead to greater impulsive trading and detriment? There is also the risk of market fragmentation if only some exchanges adopt extended hours, drawing liquidity away from others during the core session.

The SEC must also consider systemic risk. The famous “overnight gap risk” exists partly because institutional risk managers are actively monitoring positions during market hours. In a 23-hour market, risk events can unfold continuously, requiring constant global monitoring. The potential for a crisis to develop and spiral outside of traditional U.S. working hours is a legitimate concern for financial stability. The SEC’s review process will be exhaustive, likely involving multiple public comment periods to gauge input from all market participants. The approval, if it comes, may be conditional, requiring robust pilot programs and stringent reporting from Nasdaq on liquidity, volatility, and incident response during the extended hours.

Implications for the Global Financial Ecosystem

The ripple effects of a 23-hour U.S. equity market would be felt worldwide. First, it would force other major exchanges, like the New York Stock Exchange and Cboe, to follow suit to remain competitive, leading to a de facto global standard for near-continuous trading in blue-chip stocks. International exchanges in Europe and Asia might adjust their own hours to better overlap with the new U.S. session, creating even more integrated global liquidity.

For the investment industry, the changes would be profound. Portfolio management would become a more continuous process. Earnings season would be transformed; companies could no longer time releases for after the close to allow for digestion, as the “close” would barely exist. News and research would flow constantly, and the value of real-time analysis would skyrocket. Financial media would evolve into a truly 24-hour operation. Furthermore, products like exchange-traded funds (ETFs), which track these continuously trading underlying assets, would see their arbitrage mechanisms and creation/redemption processes tested in new ways.

The Connection and Competition for Crypto Industry

The relationship between this proposal and the crypto industry is one of convergent evolution and ongoing competition. Cryptocurrency exchanges pioneered the model of perpetual, global spot trading. Their technology stacks, built for resilience and automation, serve as a proof-of-concept. Nasdaq’s move represents TradFi’s attempt to co-opt a key advantage of the digital asset world. However, this does not signal a surrender to crypto; rather, it is an effort to neutralize one of its perceived benefits within a regulated, familiar environment.

Paradoxically, success for Nasdaq could heighten competition for the crypto sector. If investors can get nearly continuous, regulated exposure to companies like Apple or Tesla, the relative appeal of speculative, volatile crypto assets for “action at all hours” might diminish for some. Conversely, it could accelerate innovation in crypto, pushing exchanges toward more sophisticated financial products—like regulated single-asset crypto ETFs trading 23 hours a day to maintain differentiation. The two worlds are on a collision course, with trading hours being just one frontier. The deeper integration may come in the form of blockchain technology for settlement, which Nasdaq also actively explores, promising to make the 23-hour settlement cycle more efficient.

Conclusion

Nasdaq’s push for 23-hour trading is a watershed moment, signaling that the architecture of public markets is not sacrosanct. It is a direct response to technological possibility and shifting investor expectations, benchmarked against the relentless pace of the cryptocurrency markets. While the path forward is fraught with operational complexity and regulatory caution, the direction of travel is clear: financial markets are moving towards perpetual accessibility.

This evolution promises greater democratization for global investors but also introduces new risks and demands for continuous vigilance. The one-hour pause proposed by Nasdaq is a symbolic nod to the old world, a brief moment of daily reset in a system that never truly sleeps. Whether this specific proposal is approved in its current form is secondary; the genie of demand for continuous trading is out of the bottle. The future belongs to markets that can provide secure, liquid, and orderly trading whenever investors demand it, blurring the lines between time zones and, ultimately, between the traditional and digital asset worlds. The closing bell, a centuries-old tradition, may soon ring for the final time.

References:

CoinCatch Team

Disclaimer:

Digital asset prices carry high market risk and price volatility. You should carefully consider your investment experience, financial situation, investment objectives, and risk tolerance. CoinCatch is not responsible for any losses that may occur. This article should not be considered financial advice.